Since 2015, the Armenian Government has announced several utility-scale solar PV projects under the Government’s support. Masrik-1 (55 MW), AYG-1 (200 MW), AYG-2 (200 MW) and a series of PV projects with an aggregated 120 MW capacity, were among those projects. However, due to various reasons, such as the liberalization of the electricity market, the Government stopped some of those initiatives in order to allocate those capacities to participants of the competitive market. In December 2024, the 55 MW Masrik-1 PV power plant was connected to the grid. In the meantime, on April 8th, the Minister of Economy announced that construction of AYG-1 solar PV plant will begin in 2026.

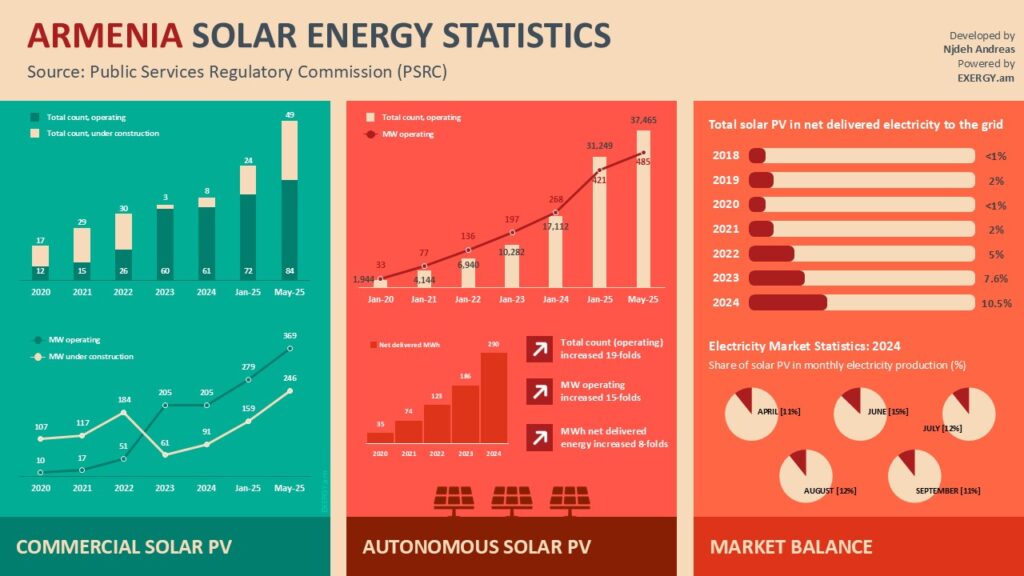

According to the public reports of PSRC, as of July 2025 there are 84 commercial solar PV plants with total 369 MW installed capacity operating in Armenia, of which 62 plants (260.4 MW) operate under the Power Purchase Agreement (PPA) scheme, whereas 22 plants (108.7 MW) operate without a PPA. In the meantime, 49 commercial solar PV plants with total 245.5 MW capacity are under construction. Table 1 summarizes the latest statistics on commercial solar PV plants.

The share of solar PV in Armenia’s electricity mix

In the RA Energy Sector Development Strategic Program to 2040 the Armenian Government has set ambitious target of increasing the share of produced solar photovoltaic energy in the energy balance up to 15% by 2030. According to PSRC’s annual reports, in 2014, the share of solar PV plants (including both commercial and autonomous) in the annual electricity mix was around 8.5-percent (776.62 million kWh from the total 9,187.14 million kWh electrical energy generation). In June 2024, 15-percent of the overall electrical energy was produced by solar PV power plants. While solar PV power production reaches its peak in June and August, such increase in the share of solar PV plants in the overall electricity mix is due to the major overhaul of the Armenian Nuclear Power Plant during June and July, along with a reduced power production capacity by large hydropower plants.

The share of solar PV power generation in the overall electricity mix has surged from 0.07 percent in 2018 to 8.5 percent in 2024. These figures exclude self-consumption by autonomous power producers and reflects only the electricity injected into the grid by these producers. Assuming that annual electricity generation from other technologies remains constant in the coming years, the commissioning of 49 commercial solar PV plants currently under construction along with 518 autonomous solar PV plants will increase the share of solar PV in the total electricity mix to over 17 percent.

Critical questions to be asked

Encouraging as these trends are, they raise the following critical questions:

- Is the existing legal and regulatory framework sufficient to manage such rapid growth?

- Can the transmission and distribution networks absorb the increasing share of variable solar generation?

- Do grid codes and interconnection standards need to be updated to maintain reliability?

- How are balancing, ancillary services, and storage being integrated into system planning?

- Are data collection and monitoring systems robust enough to assess the real-time impact of distributed PV?

- How can we mitigate risks of overcapacity or unsustainable investment bubbles?

- Are financial institutions and consumers adequately informed and protected?

- What measures are in place for PV module recycling and waste management?

- How does rapid PV growth fit into the national energy transition strategy?

- What mechanisms ensure coordination among stakeholders — utilities, regulators, investors, and consumers?

- Is there a need to establish a capacity-building or certification system for installers and service providers?

Resources:

Quality infrastructure for PV (QI4PV) in Armenia: Presentation of gaps and proposed roadmap

Comments are closed